What Trump's Mortgage Move Means Now

#mortgage #housing #policy #economics #trump

Analyzing how President Trump's housing policy could push mortgage rates lower and affect affordability.

## Overview Fannie Mae, formally known as the Federal National Mortgage Association (FNMA), is a cornerstone of the U.S. housing finance system, operating as a government-sponsored enterprise (GSE) since its founding in 1938 during the Great Depression[2][5]. Established under the New Deal to expand the secondary mortgage market, Fannie Mae’s mission is to ensure a reliable and affordable supply of mortgage funds nationwide, supporting both homeownership and rental housing[2][5][8]. ## Core Functions Fannie Mae purchases residential mortgages from approved lenders, bundles them into mortgage-backed securities (MBS), and sells these securities to global investors[1][4]. By doing so, it injects liquidity into the mortgage market, allowing lenders to offer more loans at stable rates[1][4][5]. The organization also guarantees the timely payment of principal and interest on these securities, attracting a diverse investor base and helping to lower borrowing costs for American families[1][4]. In the first half of 2025 alone, Fannie Mae provided $178 billion in funding to the housing market and helped 668,000 households buy, refinance, or rent homes[4]. ## History and Evolution Originally a federal agency, Fannie Mae became a publicly traded, shareholder-owned company in 1968, though it retains a congressional charter and operates under federal oversight[2][5]. Its “sibling” organization, Freddie Mac, was created in 1970 to further support the mortgage market[5]. Over the decades, Fannie Mae has played a pivotal role in standardizing mortgage underwriting, pioneering automated underwriting systems (such as Desktop Underwriter), and expanding access to credit for underserved communities[4]. ## Current Status and Key Metrics As of mid-2025, Fannie Mae remains one of the largest financial institutions in the world, with over $4.3 trillion in total assets and a net worth of $101.6 billion[

#mortgage #housing #policy #economics #trump

Analyzing how President Trump's housing policy could push mortgage rates lower and affect affordability.

#trump #fannie_mae #freddie_mac #housing #privatization

President Trump has announced plans to release Fannie Mae and Freddie Mac from government control, sparking excitement and speculation in the housing industry.

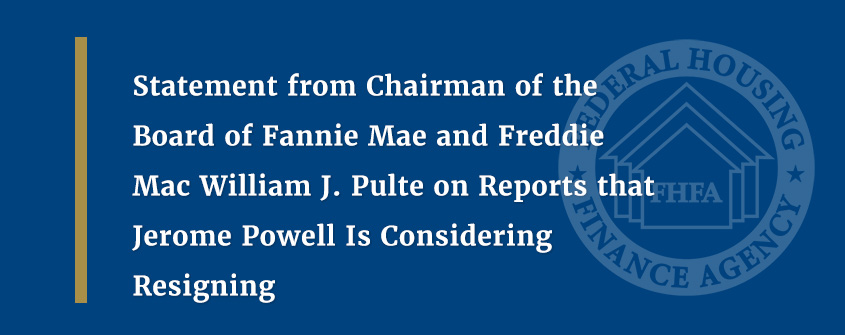

#fannie_mae #federal_reserve #economy

William J. Pulte, Chairman of Fannie Mae, expresses support for Jerome Powell potentially resigning as Federal Reserve Chair and the positive impact it could have on the economy.